Premium

Download

Edit

Download

Edit

Download the Supply and Demand Facts & Worksheets

Click the button below to get instant access to these worksheets for use in the classroom or at a home.

Download This Worksheet

This download is exclusively for KidsKonnect Premium members!

To download this worksheet, click the button below to signup (it only takes a minute) and you'll be brought right back to this page to start the download!

Sign Me Up

Edit This Worksheet

Editing resources is available exclusively for KidsKonnect Premium members.

To edit this worksheet, click the button below to signup (it only takes a minute) and you'll be brought right back to this page to start editing!

Sign Up

Not ready to purchase a subscription? Click to download the free sample version Download sample

Download This Sample

This sample is exclusively for KidsKonnect members!

To download this worksheet, click the button below to signup for free (it only takes a minute) and you'll be brought right back to this page to start the download!

Sign Me Up

Table of Contents

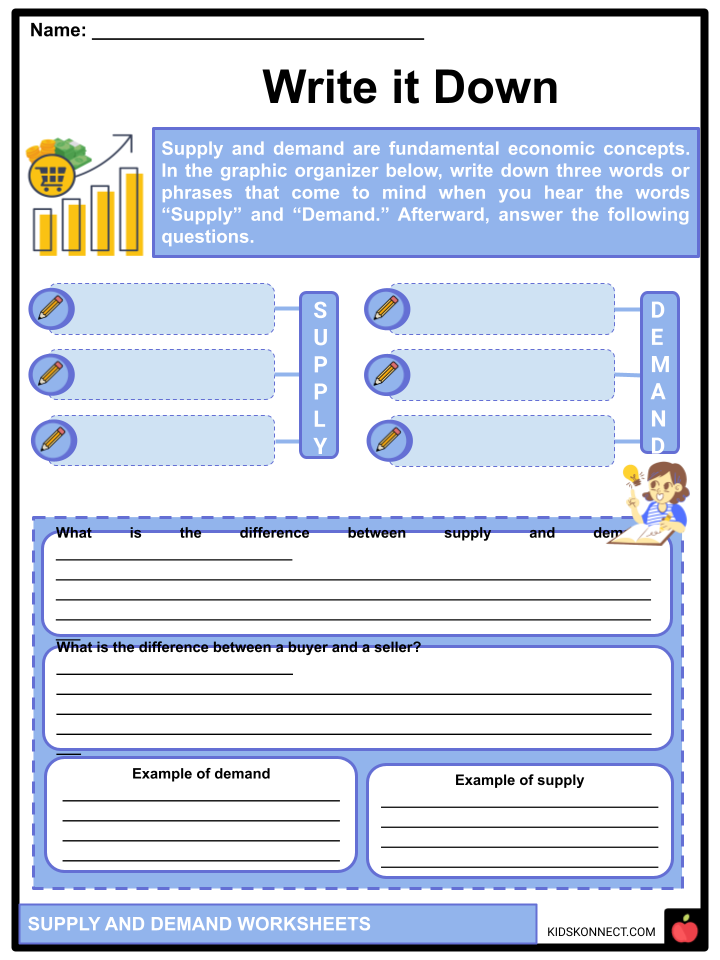

The concept of Supply and Demand is fundamental to the discipline of economics. These two forces are influenced by the price, which determines the quantity of supply and demand. Supply is the number of products and services that a seller is willing and able to produce. Demand is the number of products and services that consumers are willing and able to buy.

See the fact file below for more information on Supply and Demand, or you can download our 29-page Supply and Demand worksheet pack to utilize within the classroom or home environment.

Key Facts & Information

DEFINITION

- Supply is an economic concept that pertains to the number of products and services a seller can produce for market consumption. An example of supply is the number of available vegetables, fruits, and meats in the market offered by the sellers. A seller is a person or entity such as a government, cooperative, corporation, or company that provides such commodities to consumers.

- Demand is an economic concept that pertains to the number of products and services that a buyer is willing and able to acquire at a given price. An example of demand is the amount of the desired product we buy from a seller that suits our budget or financial resources. A buyer is an individual who purchases or acquires such commodities from a seller.

THE LAW OF SUPPLY AND DEMAND

- The law of supply and demand describes how the price of a product or service affects its supply and demand in the market.

- The law of supply states that, as the price of a product or service increases, the quantity supplied increases. On the other hand, a decrease in the cost of a product or service leads to a reduced amount provided. This is because the higher market price of a commodity encourages sellers to sell larger quantities of products or services in the market to gain more profit.

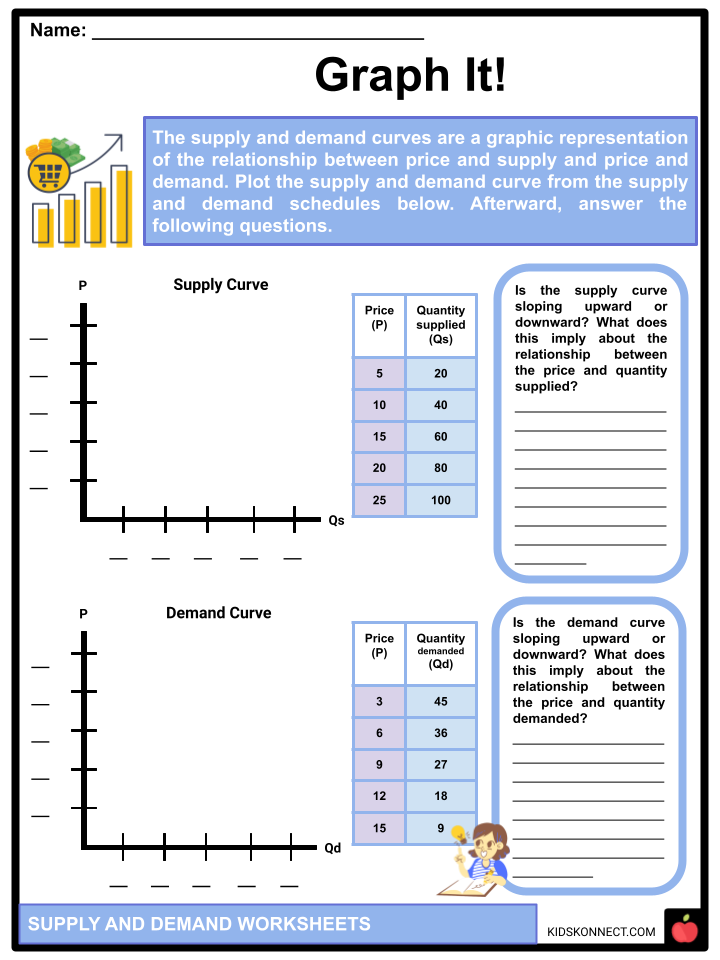

- The relationship between price and supply is illustrated in the supply curve above. A supply curve is a graphical presentation that forms an “upward sloping curve,” which indicates a positive or direct relationship between price and quantity supplied.

- In contrast to the law of supply, the law of demand states that, as the product price increases, the quantity demanded decreases. On the other hand, a reduction in prices of products and services leads to an increased amount demanded. This is because higher commodity market prices limit consumers from acquiring larger quantities of products and services.

- The relationship between price and demand is illustrated in the demand curve above. A demand curve is a graphical presentation that forms a “downward sloping curve,” which indicates an inverse relationship between price and quantity demanded.

MOVEMENT ON THE SUPPLY AND DEMAND CURVE

- Movement on the supply curve denotes that there are changes in price that cause changes in the Quantity supplied (Qs). In this case, only changes in prices affect the changes in Qs.

- Likewise, movement on the demand curve implies that there are changes in price that cause changes in the quantity demanded (Qd). In this case, only changes in prices affect the changes in Qd.

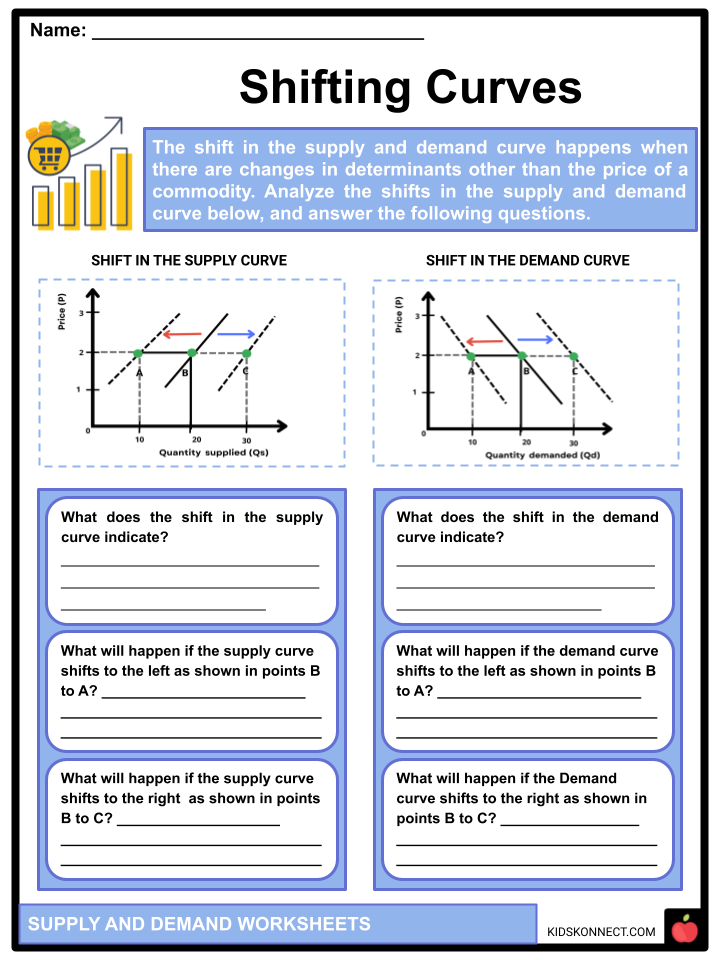

SHIFT IN THE SUPPLY AND DEMAND CURVE

- A shift in the supply curve occurs when there are changes in quantity supplied (Qs), even if the price remains constant. In this case, changes in Qs are affected by factors other than price: determinants of supply.

- Similarly, a shift in the demand curve occurs when there are changes in quantity demanded (Qd), even if the price remains constant. In this case, changes in Qd are affected by other factors than price: determinants of demand.

DETERMINANTS OF SUPPLY

- Determinants of Supply are the factors that may affect the supply of a specific commodity in the market. Below are the determinants of supply:

- Number of Sellers. An increase in the number of sellers offering a specific product or service in the market will lead to an overall increase in the supply of such commodities.

- Price of Commodity. The cost of commodities in the market vastly influences its supply. If the price of a particular product or service increases, there will be an increase in its collection, as the sellers are encouraged to provide these commodities in return for higher profit.

- Cost of Production. An increase in the prices of raw materials leads to a rise in the overall cost of production. This results in a decrease in the supply of such commodities in the market.

- Technology. Machinery used in production helps to increase the number of produced products in a given period. This leads to an increase in the supply of such commodities in the market.

- Government Intervention

- Taxes- The taxes imposed by the government cause an overall rise in the cost of production, which leads to a decrease in output and supply of commodities in the market.

- Subsidies- Financial assistance given by a government to business owners decrease the cost of production. This leads to increased output and supply of commodities in the market.

- Expectations. Expectations of sellers in the future price of the commodity they offer to affect the present supply of such commodities in the market. If a seller expects that the cost of the product they sell will increase next week, the seller will hoard the product at present and sell it next week at a higher price. Thus, the supply of such products in the market will decrease at the present time.

DETERMINANTS OF DEMAND

- Determinants of Demand are the factors that may affect the demand for a specific commodity in the market. Below are the determinants of demand:

- Price of Commodity. The cost of a commodity relatively affects the demand. If the price increases, the demand will decrease. Conversely, if the price decreases, the demand will increase.

- Income of Buyers. Income determines the capacity of people to acquire such goods and services. If the payment of consumers increases, the demand increases. Similarly, if the income of the consumers decreases, the demand will also decrease.

- Prices of Related Goods

- Substitute goods- If the price of a product increases and its substitute good has a lower price, the demand for the product will decrease, and the demand for its substitute will increase. For instance, if the price of butter rises, its demand will decrease, while the demand for margarine which is its substitute, will increase.

- Complementary goods- These are products purchased together with a particular good. An example of this is coffee and creamer. If the price of coffee increases, its demand will also decrease together with the demand for its complementary good, which is creamer.

- Taste and Preferences of Buyers. The desire and preference of consumers for a particular product or service available in the market determines its demand. If most consumers prefer or desire the product, its demand will increase, and vice versa.

- Expectations. If the consumer expects an increase in the price of a product in the future, they demand more of it in the present, and vice versa. For instance, if there is an announcement of a price increase in gasoline for next week, consumers will buy additional liters of it to save money. Thus, the demand for gasoline increased.

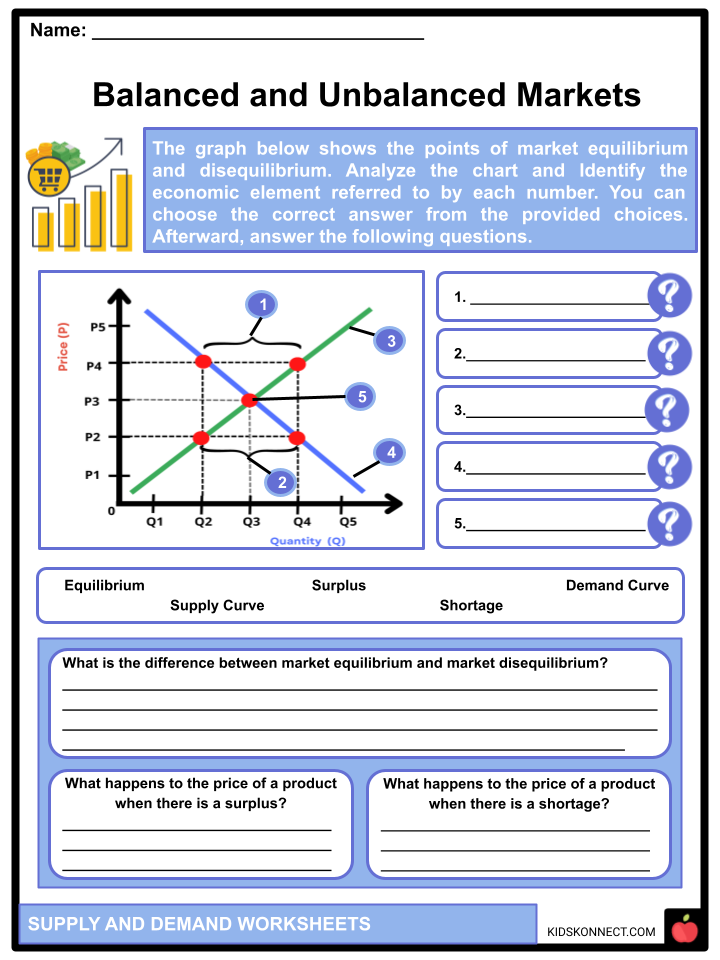

MARKET EQUILIBRIUM AND DISEQUILIBRIUM

- Market equilibrium is a state where economic forces are balanced: this happens where the quantity supplied and the quantity demanded are equal. The left graph above shows a market equilibrium, where the supply and demand curves intersect in a combined price and quantity. P3 is the equilibrium price, and Q3 is the equilibrium quantity.

- Equilibrium price refers to the price at which the quantity supply matches the demand.

- On the other hand, equilibrium quantity refers to the point at which the quantity supply of a good matches the quantity demand.

- In contrast to market equilibrium, market disequilibrium is a state with imbalanced supply and demand. The quantity supplied is greater than the quantity demanded which causes a surplus or the quantity demanded is greater than the quantity supplied causing a shortage. Excessive quantity supply of particular goods pressures sellers to drop the price of the product while the surplus lasts.

- Surplus is a market situation where there is an excessive quantity supply of a particular product or commodity. This happens when the price is above the equilibrium price. Thus, the sellers are pressured to drop the price of the product to eliminate the surplus.

- Shortage is a market situation where there is an excessive quantity demanded of a particular good. It happens when the price of a good is below the equilibrium price. This market phenomenon causes upward pressure on the price of specific goods.

Supply and Demand Worksheets

This is a fantastic bundle that includes everything you need to know about Supply and Demand across 29 in-depth pages. These are ready-to-use worksheets that are perfect for teaching kids about Supply and Demand, which are the two fundamental forces in economics influenced by price.

Complete List of Included Worksheets

Below is a list of all the worksheets included in this document.

- Supply and Demand Facts

- Write it Down

- ECONcept Hunt

- Predicting Demand

- Supply Examples

- Graph It!

- Moving Curves

- Shifting Curves

- Determining Determinants

- Changing Factors

- Balanced and Unbalanced Markets

Link/cite this page

If you reference any of the content on this page on your own website, please use the code below to cite this page as the original source.

Link will appear as Supply and Demand Facts & Worksheets: https://kidskonnect.com - KidsKonnect, October 20, 2022

Use With Any Curriculum

These worksheets have been specifically designed for use with any international curriculum. You can use these worksheets as-is, or edit them using Google Slides to make them more specific to your own student ability levels and curriculum standards.